Fixed vs Variable Mortgage Rates: What Ontario Buyers Should Choose in 2025?

Updated: June 2025

Choosing between a fixed vs variable mortgage in Ontario can be difficult, especially with today's changing interest rates. The fact that 85% of mortgages were taken out when interest rates were at or below 1% means that many Ontario homebuyers may experience payment shock when their mortgages are renewed in 2025. This guide breaks down the best type of mortgage Ontario 2025 options to help you make the right choice.

Understanding Your Mortgage Options in Ontario

Fixed Rate Mortgages

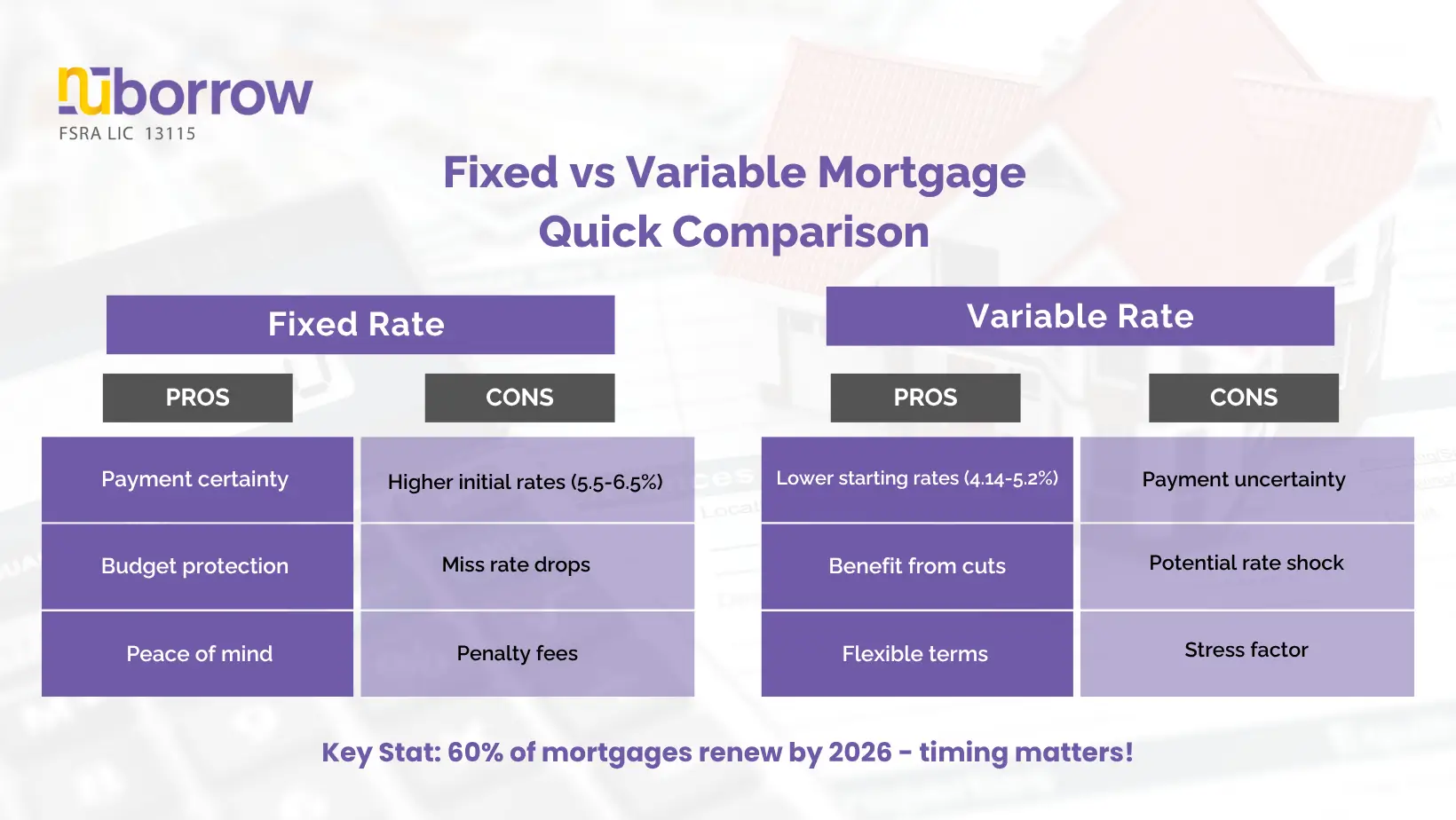

With fixed mortgages, your interest rate is fixed for the entire duration of the loan. It's easy to make a budget because your monthly payments remain constant. The majority of Ontario buyers opt for stable 5-year fixed terms.

Variable Rate Mortgages

The policy rate set by the Bank of Canada affects variable rates. By the end of 2025, at least two additional 25 basis point reductions are anticipated by economists, which may bring prime rates down to about 4.45% from the present policy rate of 2.75% and prime rate of 4.95%. This makes variable mortgages an attractive option for risk-tolerant purchasers.

Fixed vs Variable Mortgage Quick Comparison.webp">

Fixed vs Variable Mortgage Quick Comparison.webp">

Ontario Land Transfer Tax Rebate and Mortgage Decisions

Ontario's land transfer tax rebate helps first-time buyers save up to $4,000. This rebate can impact your mortgage choice: **Lower upfront costs **require more cash for a larger down payment **Lower upfront costs ** give you more freedom to select the terms of your mortgage First-time buyer programs go well with competitive mortgage rates For homes worth over $368,000, the rebate offers the greatest advantage because homes under this level are eligible for a complete refund with no land transfer tax paid.

Should I Choose a Fixed or Variable Mortgage in 2025?

Current Market Conditions

In Canada, mortgage rates today range from 4.14% to more than 6.5%, and the difference between fixed and variable rates is smaller than it was in previous years. This makes the decision more difficult.

Interest Rate in Ontario:

Current Bank of Canada policy rate: 2.75% Current prime rate: 4.95% By the end of 2025, economists estimate that the prime rate might drop to about 4.45% By the end of 2026, around 60% of outstanding mortgages will be renewed

Steps to Choose the Right Mortgage in Ontario

1. Assess Your Risk Tolerance

Can you handle payment increases? Although they demand flexibility, variable rates have the potential to save money.

2. Review Your Budget

Calculate maximum monthly payments you can afford if rates increase by 2-3%.

3. Consider Your Timeline

Staying in your home for 5+ years? Fixed rates provide certainty. Planning to move sooner? A variable might save money.

4. Get Pre-approved

Compare rates from multiple lenders. Credit unions and online lenders usually offer competitive rates.

5. Consider Rate Holds

It's a good time for mortgage shoppers to get a rate hold while you house hunt.

Pros and Cons for Ontario Buyers

Fixed Rate Mortgages

Pros:

- Predictable monthly payments

- Prevent rate increases

- Smart and simpler budgeting and planning

Cons:

- Higher initial rates

- If rates decline, you will miss out.

- Early termination penalties

Variable Rate Mortgages

Pros:

- Lower initial rates

- Benefit from rate decreases

- More flexible terms

Cons:

- Payment uncertainty

- Stress from rate changes

- Potential payment shock

Frequently Asked Questions

What's the difference between fixed and variable mortgages?

Variable mortgage rates change based on Bank of Canada policies and market conditions, whereas fixed mortgages have a constant interest rate for the duration of the loan.

Are variable rates expected to drop in 2025?

Yes, it is anticipated that variable rates will decrease to about 4 percent in 2025, but they will still be higher than average.

In Ontario, what kind of mortgage is more common?

Nowadays, a lot of buyers in Ontario, particularly those refinancing from ultra-low-rate mortgages, prefer fixed rates since they are stable.

Can I switch my trem from variable to fixed?

Most lenders permit conversion from variable to fixed, but not the other way around. Check your mortgage terms for specific conditions.

How does the Bank of Canada's rate affect my mortgage?

Bond markets and lender funding costs have an impact on fixed rates, whereas changes in the Bank of Canada directly affect variable rates.

Final Thoughts

The choice between fixed vs variable mortgage in Ontario in 2025 depends on your personal situation, risk tolerance, and market outlook. Both approaches have value as rates are anticipated to stabilize and possibly decline. When making this critical decision, keep your financial goals, timeline, and comfort with uncertainty in mind.

Contact Nuborrow today for personalized advice and competitive rates tailored to buy your home in Ontario.